A case study on the impact that Digital Identity of Devices can bring for OEM and OES in the Automotive Aftermarket Industry

The automotive aftermarket is the secondary market of the automotive industry, concerned with the manufacturing, re-manufacturing, distribution, retailing and installation of all vehicle parts, chemicals, equipment, and accessories, after the sale of the automobile by the original equipment manufacturer (OEM) to the consumer. The parts, accessories, etc. for sale may or may not be manufactured by the OEM.

Why Automobile Aftermarket is a lucrative market?

- Global vehicles in operation are expected to increase sharply over the 2016-2022 period driving the market of aftermarket products.

- The Global Automotive Aftermarket was USD 643.10 billion in 2016 and is estimated to reach USD 847.15 Billion by 2022, at a CAGR of 4.7% for the forecasted period

- Global Passenger Car Accessories Market to Mark a Revenue of USD 394.5 Billion by 2023

The Current Scenario

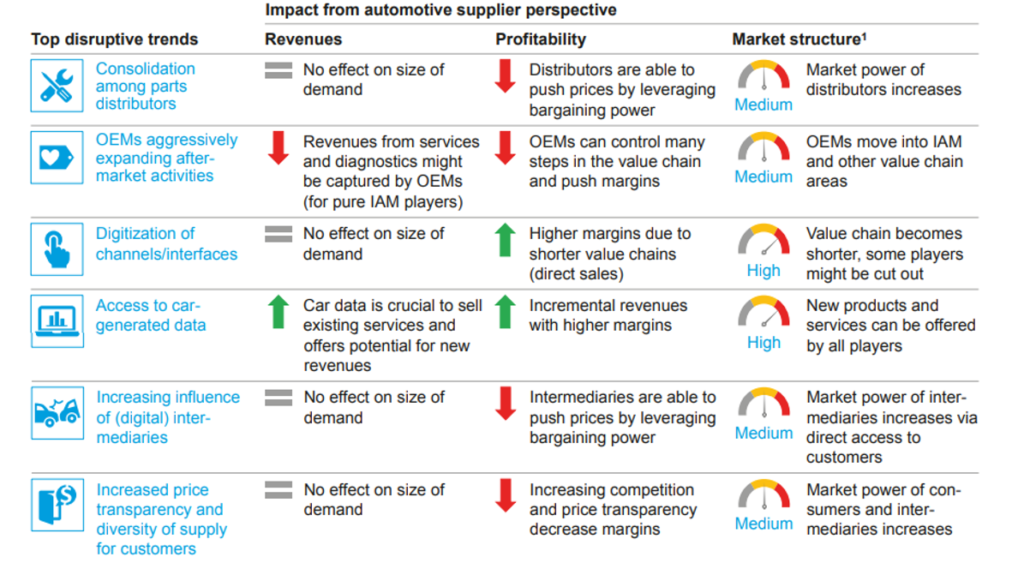

- OEMs and OESs face significant price competition from copy manufacturers

- OEMs’ parts revenue is expected to decline in the next three years, indicating that margins could come under increased pressure.

- On the demand side of standard high-volume parts, specialty chains and fast fitters such as KwikFit, PitStop and A.T.U. will benefit and have more power to negotiate prices

- Independent vendors, supplying, for example, Bosch Repair Centers, may also increasingly replace OEMs in the aftermarket. These shifts may result in lower prices for standard and high-volume parts by 10% to 15% in the next five years. This means that most market players except for copy manufacturers and specialty chains will face a reduction in overall turnover.

- Presence of local manufacturers and lack of standards and regulations is leading the players to manufacture low-quality passenger car accessories. This increasing number of low quality offerings of passenger car accessories is hampering the growth of industry and decreasing the revenue share of the organized players.

- An of course the threat of counterfeit spare parts delivered in the grey market and unbranded repair shops and service centers.

High Competition faced by OEM/OES in the Automotive Aftermarket

- OEMs and OESs face significant price competition from copy manufacturers

- OEMs’ parts revenue is expected to decline in the next three years, indicating that margins could come under increased pressure.

- On the demand side of standard high-volume parts, specialty chains and fast fitters such as KwikFit, PitStop and A.T.U. will benefit and have more power to negotiate prices

- Independent vendors, supplying, for example, Bosch Repair Centers, may also increasingly replace OEMs in the aftermarket. These shifts may result in lower prices for standard and high-volume parts by 10% to 15% in the next five years. This means that most market players except for copy manufacturers and specialty chains will face a reduction in overall turnover.

- Presence of local manufacturers and lack of standards and regulations is leading the players to manufacture low-quality passenger car accessories. This increasing number of low quality offerings of passenger car accessories is hampering the growth of industry and decreasing the revenue share of the organized players.

- An of course the threat of counterfeit spare parts delivered in the grey market and unbranded repair shops and service centres.

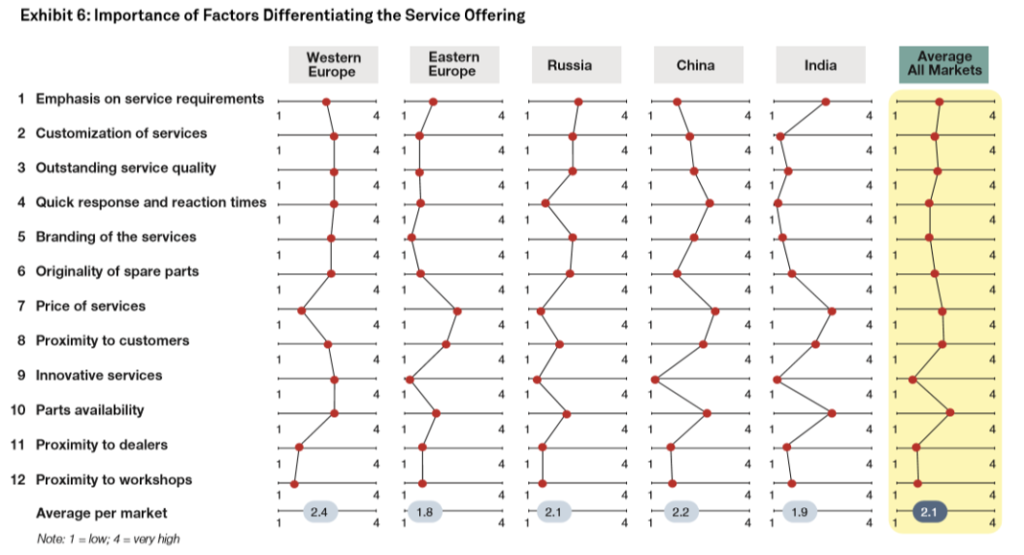

Varying Customer Expectations across Regions

As per a research conducted by CapGemini the main differentiating factors vary from region to region but broadly they are parts availability, proximity and originality along with price, specific requirements and innovative service.

- In Western Europe, the main factors for differentiating the service offerings are innovative services, the high emphasis on specific customer requirements and customization of services. In line with the importance of customization, proximity to customers and offering services for attractive prices play an important role as well

- Russia is particularly demanding when it comes to branding of services. Prices are not considered to be a differentiator for service offerings as price sensitivity for services seems to be relatively low. More important is that reasonable prices are in line with sophisticated service quality and close proximity to customers.

- In China, the price of services is the most important factor to achieve market differentiation. However, besides attractive prices customers request quick response and reaction times and sufficient service quality.

- India seems to be the least ambitious market in terms of differentiation. Neither service innovation, service quality, branding nor service levels seem to offer significant differentiation opportunities. The most important ways to achieve differentiation are service price and availability of parts. Furthermore, there seem to be specific service requirements that are most relevant to Indian consumers. Emphasizing these specific requirements is a potential way to achieve differentiation.

The Indian Aftermarket Scenario

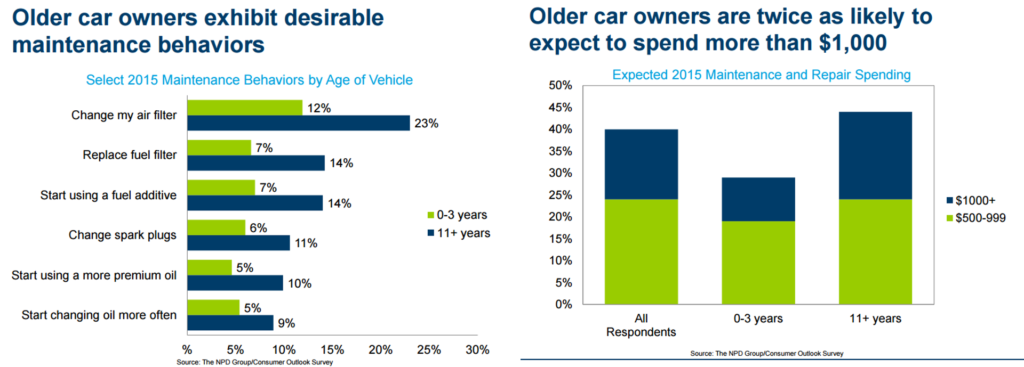

- In India, according to ACMA while nearly 20% of the cars on road are more than 15 years old, the typical age profile of cars reporting at dealerships is of less than seven years.

- This means that the older the car, the less likely the car visits the OEM service centre. Once the car changes hands, this is even less likely. But the irony is that the older the car grows, more is the need for service and parts.

- Industry studies pegs the current size of the components business in the Indian automotive after-market between USD 280 – USD 300 billion (of this 26 per cent is accounted for by cars), whereas the service market is estimated at USD 80 Billion. The combined value is projected to rise to USD 600 billion by 2020.

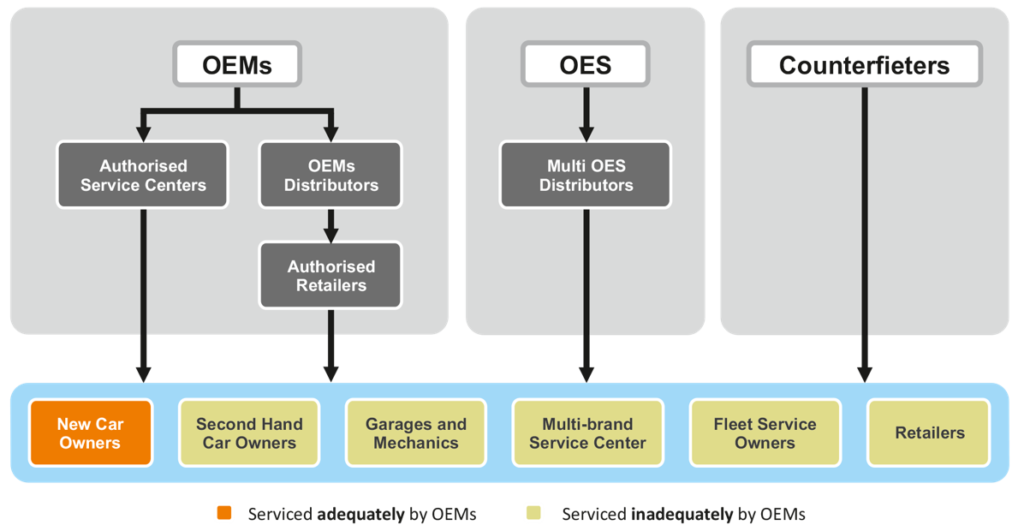

- Many car manufacturers do not have complete reach either through their service centers or through their distributors to cater to a fast expanding aftermarket.

- Even the suppliers of the OEMs who have the freedom to supply to this market very rarely have the capability to do an effective distribution. Since this means that parts of many of the car brands are not freely available in the market, the situation creates an unmet need in the market opening up an oft unacknowledged channel – leak of parts from dealerships and service centers into the open market

- It is also seen that many OEMs have targets for parts sales for its service centers. In these cases too, it becomes in the best interest of the service center to push some of their monthly target into the open market. This will often be at a lower price since the attempt is to either clear inventory or to sell in bulk. The best intentions of the OEM are thus defeated while simultaneously taking a hit to the bottom line.

- One of the prime reasons for significant counterfeit sales in spare parts is because of poor availability of parts. No other consumer product category has seen counterfeiting to this extent in the Indian market. ACMA assesses that 36% of the components in the aftermarket are fake. It is also thought to be growing 9-11% annually. Since counterfeiting is usually of the OEM’s intellectual property, in addition to eating into the aftersales of the car manufacturer, it may also spoil the car and endanger the life of the owner.

- A new segment of fleet operators and taxis that tend to be demanding in a) price b) reliability c) quality and d) safety is evolving into a relevant segment. In recent years this segment has grown substantially to over 500,000 cars on the road. The larger among them even have their own service centers. In addition to price competitiveness, reliability in availability of the required part at the right time at the required place is of crucial interest to them! If there are long periods of waiting to source parts from the OEMs and their distributors, they will look for alternatives

The Solution

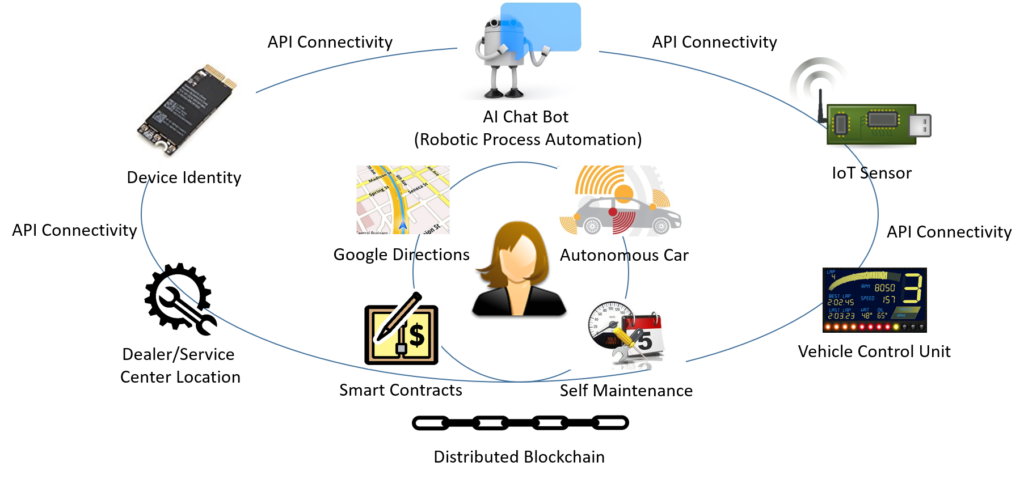

How Device Identity & Connectivity can drive Competitive Advantage & Outreach

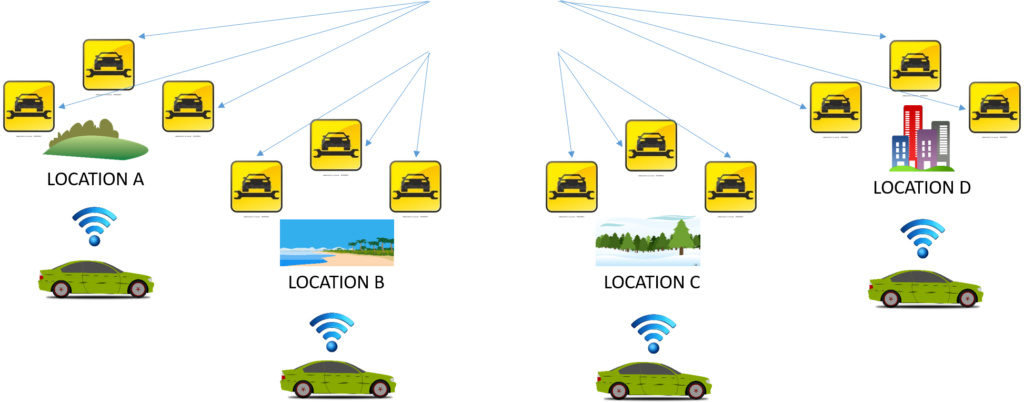

- Self Identification of replacement needs (Car Data) is announced or communicated to the customer directly through in-car computer systems communicating with device sensors

- The faulty or replaceable device identity is tracked and an automatic localized search for authorized dealer and OES network based on the identified device is made, enabling repair/replacement to be done quickly and locally

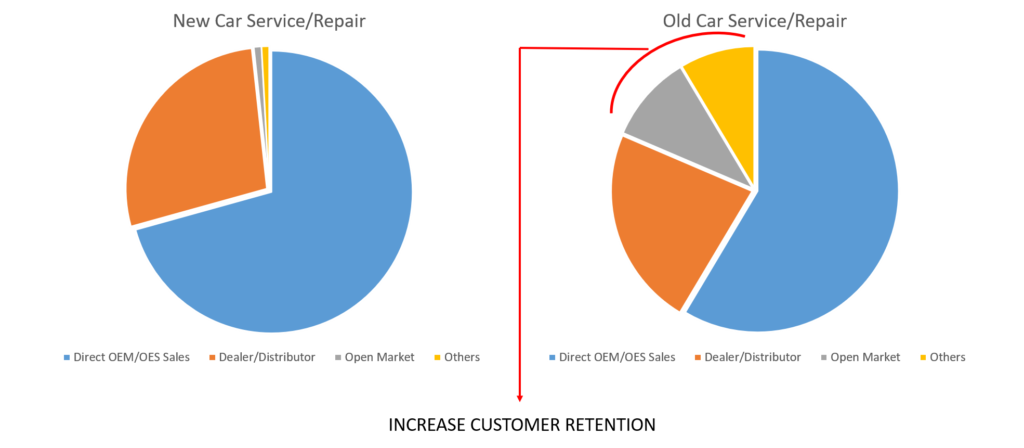

- Customers do not need to look anywhere as problem identification and replacement decision takes place within the car itself thus increasing overall customer retention.

- Only authentic spare parts and authorized dealer and OES network based on customer location is matched by the system based on the device identity thus reducing the chance for a customer to search in the open market which decreases overall competition.

- Mapping of the customer profile with driving behaviour will help generate potential for upsell of product and services

- Maintenance schedules and replacement alerts can be communicated to the service centre beforehand thus leading to efficient service delivery and ensuring spare part availability. (The service centre essentially knows who is coming and what to expect from his car)

- The OEM can build a clear demand forecast picture overtime based on localized, and seasonal needs and thus can plan his spare parts production schedule with logistics and distribution plan .

- Gradually the OEM can move towards building small, smart and localized factories taking care of local demands and de-centralizing the entire process.

The Value Impact of Digital Identity

Increased Customer Retention

Localization & Availability

The Future

A world where the customer and the car are interlinked each understanding and fulfilling their needs via a fast, seamless and secure connectivity network. Cars, manufacturers, dealers, devices and customers are all connected with super-efficient, customized and localized service.

As per a recent McKinsey survey the aftermarket industry shows that the highest impact on aftermarket sales and profitability will result from digitization and inter-connectivity of services with car generated data.

Remember the TV series Knight Rider … Michael and his advanced artificially intelligent, self-aware, self piloting and nearly indestructible car. That is now not too far from reality.

We are truly entering a global connected world where humans and device co-exist for the betterment of our society, lives and environment

0 Comments